How can you make your bank’s customers control transactions on their accounts and use it as an effective fraud protection mechanism? Customer communication and preferences can be vital in detecting fraud early and costs far less.

Consider the following scenarios:

- A customer is going on vacation to Switzerland for 2 weeks and he wants all the card transactions (debit card and credit card) originating from home country to be blocked for the next two weeks.

- Customer wants all fund transfer (Third Party transfer) transactions originating from his internet banking account at any location in home country to be blocked for next 2 months as he is travelling to US for business.

- Customer runs a domestic business and doesn’t travel abroad. The customer wants to disable any transaction originating abroad.

- Customer wants all payee addition transactions to be blocked in his account till he turns this feature on (aka Facebook privacy settings).

- Customer wants to be alerted of any attempt of transaction of more than a set limit with the option to respond with a decision to decline or authorize the transaction (aka. reverse positive payee used for cheque transactions in the commercial banking world).

- Customer holds multiple credit cards and uses a specific credit card for all his ‘Card Not Present’ transactions (online payments). Customer wants all the CNP transactions to be blocked on all his other debit/credit cards.

- Customer wants to block or fix specific limits for purchase of electronic or jewelry items on his debit/credit card.

- Customer wants to limit the use of his debit card/credit card to any particular state/states within the country.

In all these scenarios, the bank customers provide the vital situational intelligence which can be built into the banks’ processes for effective fraud protection. In turn, customers also benefit with the convenience of banking on their own terms and securing their accounts.

If you think this is too futuristic, you may be wrong. Reserve Bank of India’s expert committee on customer service in banking has published recommendations to this effect (Report of the committee on customer service in banks). We might see these recommendations getting implemented by Indian banks very soon.

Bank’s core system i.e. core banking, internet banking and credit card processing systems, however modern they may be, are ill-suited to handle this kind of agility. Current generation systems can at the best match a transaction to a bank maintained blacklist and stop a transaction when an entity match occurs.

Banks need to handle this using agile fraud management system which can take this situation intelligence into consideration as part of its decision making strategy for fraud protection. What banks need is a dynamic fraud management system that can digest the relevant information about the debit blocks/limit preferences customer has opted for the given time period and the same system is used for real-time fraud protection.

A real-time fraud protection system monitors every transaction and decides whether to allow, decline or challenge based on the fraud risk system inherently derives or based on the customer provided situational intelligence. This is an example of a technology that can truly achieve the dual objectives of enhanced customer experience and improved fraud control.

How do you see your institution using customer context based intelligence for better fraud prevention?

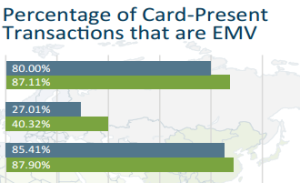

Enter EMV and NFC

Enter EMV and NFC