Cybercrime continues to be an unending botheration for banks. While the focus of attempts and attacks until recently, tended to be on the banks’ customers (via card and account detail compromises), of late fraudsters have become more sophisticated and have raised the stakes.

They have shifted their focus and are now directly targeting banks. They have begun deploying increasingly sophisticated methods of circumventing individual controls in the banks’ local environments and have probed deeper into systems to execute well-planned and finely orchestrated attacks.

One area where fraudsters have increased malicious attacks is Correspondent Banking, especially via SWIFT.

SWIFT was developed at a time when the primary focus was on interconnectivity and security was not really a concern. However, with increased adoption of the SWIFT network, security lapses / gaps in the entire value chain, especially the weaker links, have started getting exposed.

Fraudsters have discovered that they can leverage vulnerabilities in SWIFT’s member banks’ processes and procedures, particularly in countries where regulatory and security controls are less robust.

Here are a few instances –

The February 2016 SWIFT heist was a watershed moment for the payments industry. Though not the first case of fraud against a bank’s payment endpoint, it was the sheer scale and sophistication of the attack which shook up the global financial community.

The fraudsters used the following process to decamp with $81 million –

A similar modus operandi was seen in the incidents at several other banks as well – Vietnam’s Tien Phong Bank, Ecuador’s Banco del Austro and recently in an Indian private bank.

In this case the modus operandi for the SWIFT attack was on these lines –

In both cases, even though not all of the money made its way into the fraudsters’ hands, they are still alarming examples of how systems can be duped.

The success of these frauds is an outcome of a combination of factors –

Banks must counter-attack this combination in a holistic rather than a piece-meal fashion to gain an upper hand over the fraudsters. They must rally efforts on better coordinating their cyber-security, anti-fraud, and staff risk management programs.

SWIFT meanwhile has initiated a Customer Security Program (CSP), wherein it provides elaborative security controls. However, banks should put additional transaction monitoring checks using intelligent fraud detection and prevention systems. This should eliminate fraudulent cases where cyber-security systems have failed in the past.

A good enterprise fraud management system has the capability to solve most problems in the fund transfer process and prevent big ticket frauds. Some of the highlights of a multi-centric approach of a smart fraud management system are –

With cybercriminals continuing to attempt penetrating traditional strongholds, it is imperative that financial institutions take necessary steps to secure their environments. Enterprise-Wide fraud management is one of the approaches that can enable financial institutions to prevent the attacks, as well as increase the likelihood of an attack being detected in time.

![]() Recognized as bankers to the nation, and with global operations in Seychelles, Maldives, India and UK, Sri Lanka’s largest bank, Bank of Ceylon (BOC) as part of its enterprise financial crime risk management strategy has chosen CustomerXPs’ Clari5 real-time Anti-Money Laundering solution for combating money laundering threats in real-time. [Read More]

Recognized as bankers to the nation, and with global operations in Seychelles, Maldives, India and UK, Sri Lanka’s largest bank, Bank of Ceylon (BOC) as part of its enterprise financial crime risk management strategy has chosen CustomerXPs’ Clari5 real-time Anti-Money Laundering solution for combating money laundering threats in real-time. [Read More]

![]() Big data analytics and cloud storage are powering a new generation of counter-fraud tools, yielding fresh insights into deceptive behaviour and may be even wresting some advantage back from the bad actors. [Read More]

Big data analytics and cloud storage are powering a new generation of counter-fraud tools, yielding fresh insights into deceptive behaviour and may be even wresting some advantage back from the bad actors. [Read More]

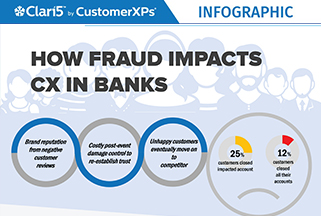

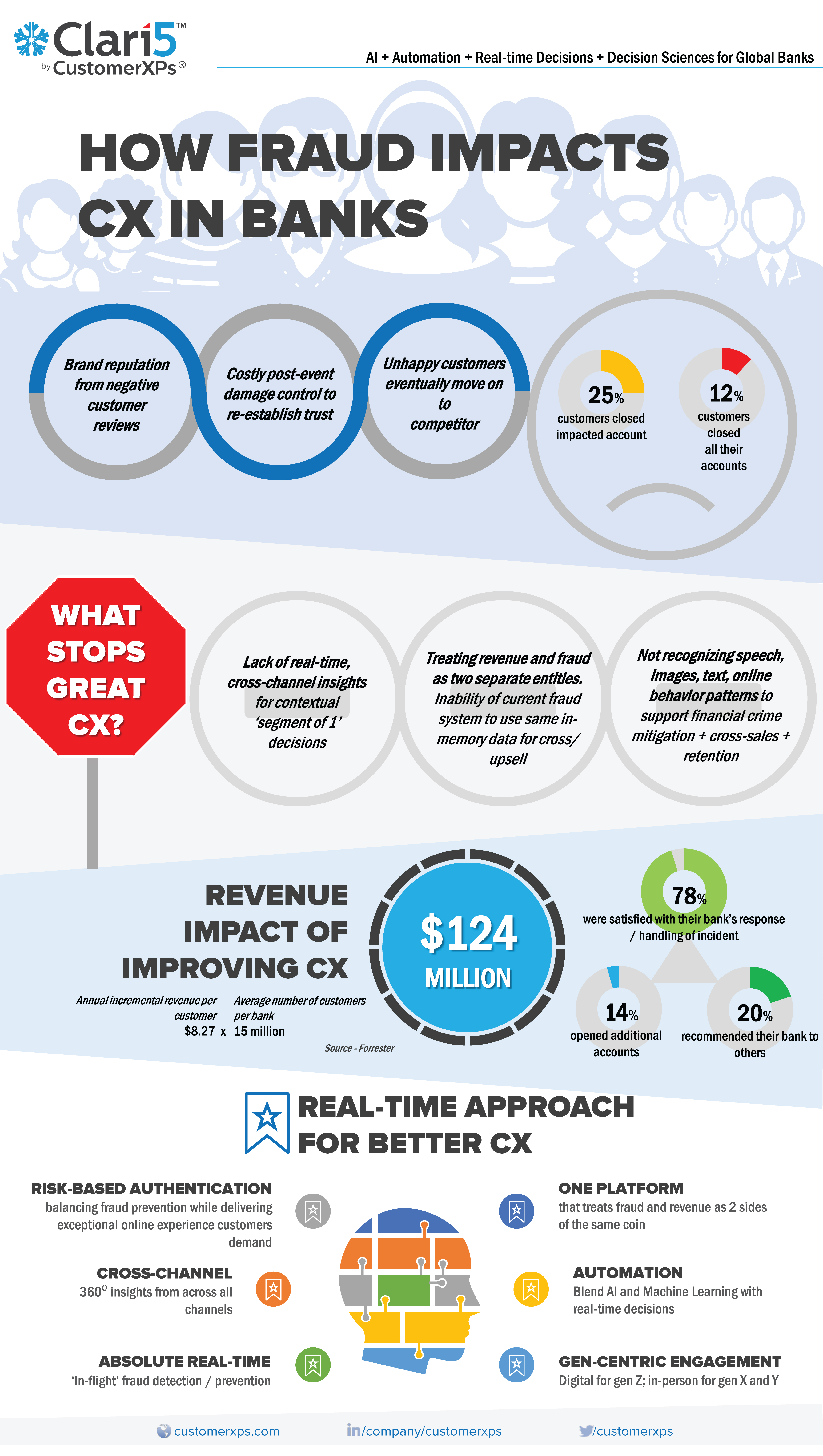

How banking fraud comes in the way of customer experience plus a few tips for superior CX.

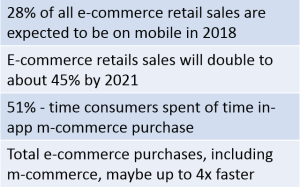

During the last holiday season, a third of all online purchases came from smartphone users. Just how central e-commerce and m-commerce (almost by default) has become to our way of life and how it’s expected to continue to grow is quite evident. According to Business Insider, e-commerce and m-commerce are showing no signs of stopping.

Mobile transactions are overtaking everything else at a rate faster than businesses can handle. With the number of consumers switching to digital and mobile channels growing literally by the hour, banks need to simultaneously boost their defense mechanisms to prevent e-commerce and m-commerce frauds.

In fact, real-time payment systems could very well be helping accelerate financial crime. A smarter mechanism to detect patterns and quickly form rules without the added complexity of software mutation and changes is essential for fraud threats to be preempted and prevented in real-time. Intelligent systems start from a basic rule and update these rules based on patterns detected from data, at incredible speeds.

Machine learning algorithms today can analyze petabytes of data in a matter of hours and detect patterns with very simple computations. The entire process of analyzing data and formulating rules can be tested, verified and validated, making this a very precise and accurate science that gets better with use. Read more on applying Machine Learning and AI in fraud detection.

But implementing AI and machine learning in banks has its own share of challenges –

The key to advanced fraud-detection is a departure from rule-based, non-predictive detection to a non-deterministic approach that can explore and detect hitherto unknown issues/ challenges. This approach relies on several areas of AI including machine learning, deep learning and cognitive computing. Using these techniques to quickly analyze huge amounts of data, analysts can create benchmarks of normal activity and behavior patterns.

But most importantly, ecommerce platforms, financial institutions and payments systems and must have the ability to instantly detect (and prevent) threats in real-time using contextual insights synthesized from across internal and external channels.

References: