Advantages of a Unified, Real-time Fraud Risk & AML Compliance (FRAML) Platform for Banks in an ‘as a Service’ model

We are excited to share that IBM LinuxONE Emperor 4 will be available globally on September 14, 2022, and Clari5 clients will have the opportunity to reduce energy consumption while reaching sustainability targets. IBM and its partners are helping clients, including those in regulated industries such as financial services, build a modern environment that is designed to improve business agility and reduce overall costs. ISVs can leverage the next generation of IBM LinuxONE’s highly secured and sustainable platform to deploy software across environments.

Banks today are overwhelmed by the number of delivery channels they need to manage. To provide a stellar digital experience, a predictable and seamless digital experience across channels is key. Banks must examine the roadblocks in the user’s path to a consistent experience and access to information across all channels. In response, banks have been heavily investing in digital transformation to achieve key objectives, including:

Clari5 is a next gen enterprise platform for real-time intelligence, using the best of technology for the most cost effective real-time intelligent solutions for financial institutions in the financial crime risk management domain.

Deployed on IBM LinuxONE and Linux on IBM zSystems, Clari5 solutions offer a wide spectrum of cross-channel and cross-product capabilities with ease of integration using a variety of mechanisms and pre-built connections.

About IBM LinuxONE Emperor 4

According to an IBM IBV study, almost half (48 percent) of CEOs surveyed across industries say increasing sustainability is one of the highest priorities for their organization in the next two to three years. However, more than half (51%) also cite sustainability as among their greatest challenges in the next two to three years, with lack of data insights, unclear ROI, and technology barriers, as hurdles.

The new IBM LinuxONE Emperor 4 is an enterprise server designed to help reduce energy consumption. For example, consolidating Linux workloads on five IBM LinuxONE Emperor 4 systems instead of running them on compared x86 servers under similar conditions can reduce energy consumption by 75%, space by 50 percent, and the CO2e footprint by over 850 metric tons annually.[1] Integrations with energy monitoring tools on the server also enable clients to track energy consumption.

Built on the IBM Telum Processor, IBM LinuxONE Emperor 4 supports data serving, core banking and digital assets workloads and is a platform of choice for organizations that value sustainability and security.

Partners with IBM Ecosystem

As a part of the IBM Ecosystem, Clari5 is helping companies unlock the value of cloud investments by implementing the tools and technologies that can help them succeed in a hybrid multicloud world. We are excited to be working closely with the IBM Ecosystem to bring new innovation to our clients. Based on Linux, customers can benefit from open standards and an ecosystem that IBM LinuxONE offers including modern DevOps and a variety of popular software. This can also help to remove operational barriers when customers deploy and manage technologies on cloud-native infrastructure.

1 Disclaimer: Compared 5 IBM Machine Type 3931 Max 125 model consists of three CPC drawers containing 125 configurable cores (CPs, zIIPs, or IFLs) and two I/O drawers to support both network and external storage versus 192 x86 systems with a total of 10364 cores. IBM Machine Type 3931 power consumption was based on inputs to the IBM Machine Type 3931 IBM Power EstimationTool for a memo configuration. x86 power consumption was based on March 2022 IDC QPI power values for 7 Cascade Lake and 5 Ice Lake server models, with 32 to 112 cores per server. All compared x86 servers were 2 or 4 socket servers. IBM Z and x86 are running 24x7x 365 with production and non-production workloads. Savings assumes a Power Usage Effectiveness (PUE) ratio of 1.57 to calculate additional power for data center cooling. PUE is based on Uptime Institute 2021 Global Data Center Survey (https://uptimeinstitute.com/about-ui/press-releases/uptime-institute-11th-annual-global-data-center-survey ). CO2e and other equivalencies that are based on the EPA GHG calculator (https://www.epa.gov/energy/greenhouse-gas-equivalencies-calculator ) use U.S. National weighted averages. Results may vary based on client-specific usage and location.

You can find additional resources about IBM LinuxONE Emperor 4 and IBM below:

Image courtesy: Sandeep Singh on Unsplash

Image courtesy: Sandeep Singh on Unsplash

The pandemic continues to have a significant socio-economic impact with cases, fatalities and intermittent related / variant outbreaks occurring.

Since early 2020, the banking industry worldwide has been bearing the impact. A substantial section of the sector’s workforce has been furloughed, with existing workers forced to telecommute. With branch visits continuing to shrink, usage of digital channels is now at an all-time high. Call volumes at contact centers have spiked with more anxious customers seeking support, and on a wider variety of issues.

The situation has put certain critical aspects of the banking ecosystem in the spotlight, especially that of digital customer experience – a vital factor during challenging times. Imperative therefore to explore how customers’ digital experiences can be made frictionless during an exceptionally difficult phase.

Understanding Digital Friction

Quite a lot of things have changed in response to the ongoing situation. So merely having/managing multiple digital channels is not enough. Banks are already overwhelmed by the number of delivery channels they need to manage. To provide a stellar digital experience, banks require to reduce some of the digital friction points that conventional approaches have created.

From mobile banking to internet banking to ATMs to contact centers to branches – customers use multiple channels to transact. Banks need to have better self-service support options to make transactions faster and more efficient, with heightened security levels and without compromising convenience.

Having a predictable and seamless digital experience across channels is key. Banks must examine the roadblocks in the user’s path to provide a superlative experience for delivering a consistent experience and access to information across all channels.

For instance, a net banking customer shouldn’t have to call the contact center for an answer to a simple ubiquitous question. Be it mobile or online banking, users should get instant answers to queries on that very channel itself. A customer using an ATM shouldn’t have to call the contact center or go to internet banking for queries. A mobile banking customer shouldn’t be made to visit a branch if formalities can be performed via mobile banking itself. In a digital era, and more importantly because of the current situation, a branch can no longer be a primary channel.

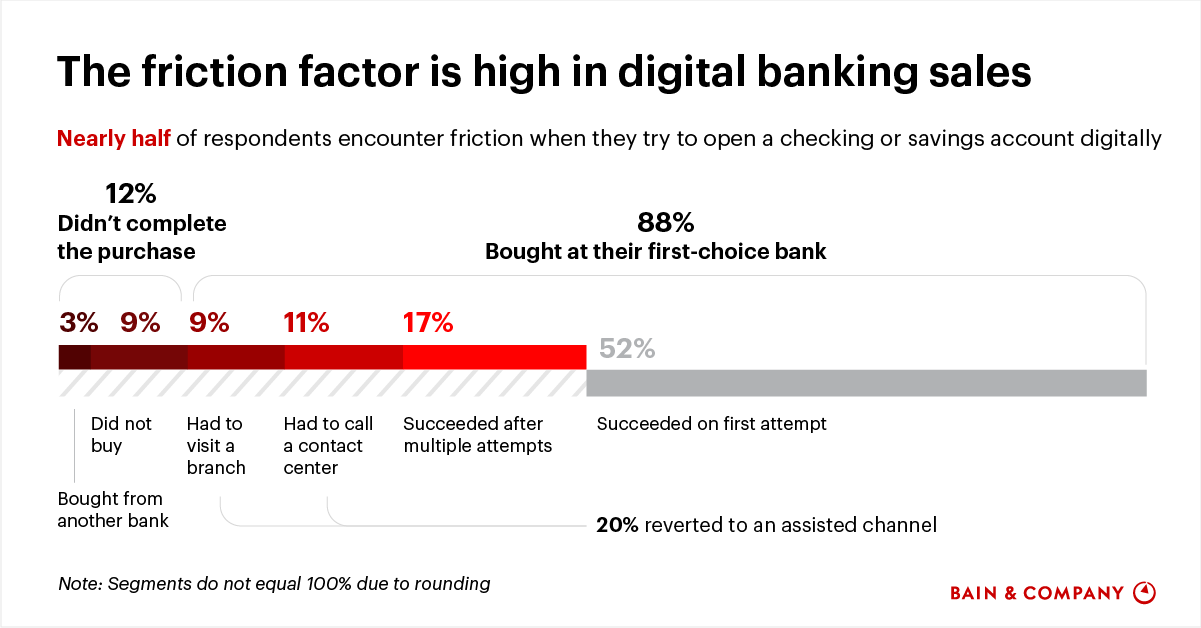

Friction escalates when inconvenient instances are compounded over time. Besides impacting customer experience, digital friction also has a domino effect – it adversely affects call volumes, productivity / efficiency levels and conversion rates. Friction is especially high in digital banking sales, with prospective customers encountering friction when trying to open a savings account (Bain & Company).

Can More Be Done To Lessen Friction?

The banking industry has never before faced such intense competition both from within and outside the industry. Even as banking becomes more unbundled, Fintech start-ups are increasing their slice of the banking pie. On the other hand, global technology giants have already moved into payment services replacing legacy organizations that had previously dominated the domain. Not so long ago, large financial institutions were competing on price and physical delivery networks. Today, digital players are competing on the same turf with CX and UX as their trump cards.

In response, banks have been heavily investing in digital transformation. We now have a variety of channels to access services anywhere / anytime. However, despite the positive trend, that vital aspect which these channels were designed to deliver, i.e., customer experience – seems to have taken a back seat.

Banks that meet changing customer expectations with personalized experiences that are fun, engaging and omnichannel can increase acquisition, engagement and loyalty and keep pace with agile Fintech competitors (CapGemini World Retail Banking Report, 2022).

However, a few banking leaders have been able to see digital transformation from a customer experience perspective and quite literally have a finger on the customer’s pulse. Going beyond basic hygiene factors, they have made it easier, faster for customers to engage, are able to anticipate customer needs and even ‘think’ for the customer.

Doing Away with Digital Friction

Digital transformation, but with minimal customer friction as the core tenet, has become a need of the hour. A few ways how banks can deliver frictionless experiences:

Better Together

A challenge faced by most banks is ownership of various channels. In most cases, IT owns mobile banking, retail ops own online banking and marketing owns the website. As a result, departments work in isolation and are not in 100% sync to provide a consistent and superior digital experience to customers. Seamless interdepartmental collaboration therefore is one of the vital factors to removing digital friction.

The Need for Speed

Make customers effortlessly navigate your digital universe – provide multiple ways for them to easily access information and perform transactions faster across all channels. Use of clear, consistent and intuitive titles – be it website, mobile, or online banking – makes it easier for customers to navigate interfaces. Adding a search functionality to enable users to find answers to their queries on the very channel they are on. Reconfigure AI-powered chatbots to answer queries in real-time instead of near real-time.

Intuitively Foreseeing The Next Move

If a digital interface knows what the customer wants or is about to do, based on behavioural analytics, it can then accelerate tasks and conveniently. The same can be achieved while increasing technology adoption by delivering a contextual ‘segment of 1’ guidance. This also helps lower contact center inquires and increase conversion rates. Financial institutions do a great job of level 1 – i.e., answer a customer’s primary question.

Step 2 involves specific next actions such as scheduling an appointment, applying online, or watching a tutorial. As step 2 anticipates the true intent behind the questions, it is critical to streamline / optimise it to reduce digital friction. For new customers, banks must implement an effective onboarding process that helps effortlessly navigate existing and new features. They must continually provide contextual support to users in research, consideration, and finalizing stage. Contextual and intuitive FAQs that anticipate common questions are effective.

Ensuring Consistent Experiences Enterprise-wide

A bank may have intuitive digital interfaces with a wealth of information available to customers. But, if the experiences are inconsistent across channels, then it contributes to increasing friction. By leveraging additional content, links, and chatbots from other digital banking platforms, banks can deliver the same access to information across all channels. Insights on customer behaviour from a particular channel can be re/cross-purposed for other channels.

Going Phygital

A portmanteau of physical and digital, phygital banking combines a variety of banking types including branch banking, mobile banking, internet banking and personalised banking. Leveraging human workforce as well as digital technology to serve customers, phygital banking blends trust with experience – both critical parameters for customers. At a time, when open banking regulations are being debated to make banks become more compliant, transparent, and data secure, phygital banking can work as a trust multiplier cum friction mitigator.

Taking The Bank To The Customer

Banking as a Service (BaaS) need not be only for rural or unbanked populace. The same concept can be applied in an urban context as well. From answering simple queries like ‘what is my savings account balance?’ or ‘transfer funds to my relative’ to helping customers in remote locations locate the nearest ATM to withdraw money during emergencies, AI-powered voice-assisted applications can help customers consume banking services with a higher experience quotient. Smart wallets monitor customer behaviour and spending trends, and then alerts / guides them on how to save more, while making smarter spending decisions.

Harnessing Machine Learning

Robust ML models can predict what customers want, before they know they want it. ML tools capable of analyzing large data sets across categories such as buying patterns, demographics, transaction volumes and service requests can help banks create targeted credit, loan or savings offers that are low-risk for banks but high-value for customers. Also, credit and loan applications historically took weeks to process.

With ML, many banks have been able to reduce timelines to days. But expectations too have increased simultaneously, with more customers demanding faster responses to sales or service queries. ML-driven application assessment and approval helps here. With access to financial data sets, ML tools can evaluate multiple credit factors and reach an unbiased decision, and do it much faster than with human involvement. Implementing ML enterprise-wide helps banks analyze / solve problems at scale. Improved ML algorithms can help banks significantly improve customer experience.

Leveraging Existing Anti-fraud Systems

Advances in real-time, cross-channel anti-fraud technology can also help provide better customer experiences even while preventing potential losses to fraud. A real-time, cross-channel anti-fraud system is already designed to synthesize contextual intelligence from across all of the bank’s delivery channels and deliver the essence of the insight in real-time within the very short transaction window for necessary intervention (i.e., allow, hold or block). However, instances of fraud are few and far in between.

The bulk of the transaction data therefore becomes a veritable goldmine of monetizable insights that can be used for instant real-time cross sell or upsell – at the precise moment when the customer is in her / his most receptive frame of mind. While the bank benefits from the advantage for generating additional revenues, customers are pleasantly surprised with the highly contextual ‘segment of 1’ interaction.

Reducing digital friction invariably tops the objectives in most banking executives research today and for a good reason. From layers of data input screens to avoidable delays in service issue resolutions, customers are bound to experience some friction or the other at some point when engaging via mobile or online. Customers simply do not have patience for sub-optimal digital experiences – many abandon transactions on at least one occasion due to friction.

Besides trust, security and data privacy, customers rightfully expect fast and frictionless digital experiences. With smooth, highly secure and intuitive experiences right from the very first interaction, banks must make frictionless experience the primary growth driver, especially during tough times. To convert satisfaction to loyalty, banks that deliver great digital experiences will be the ones that will emerge winners.

{kind=link}