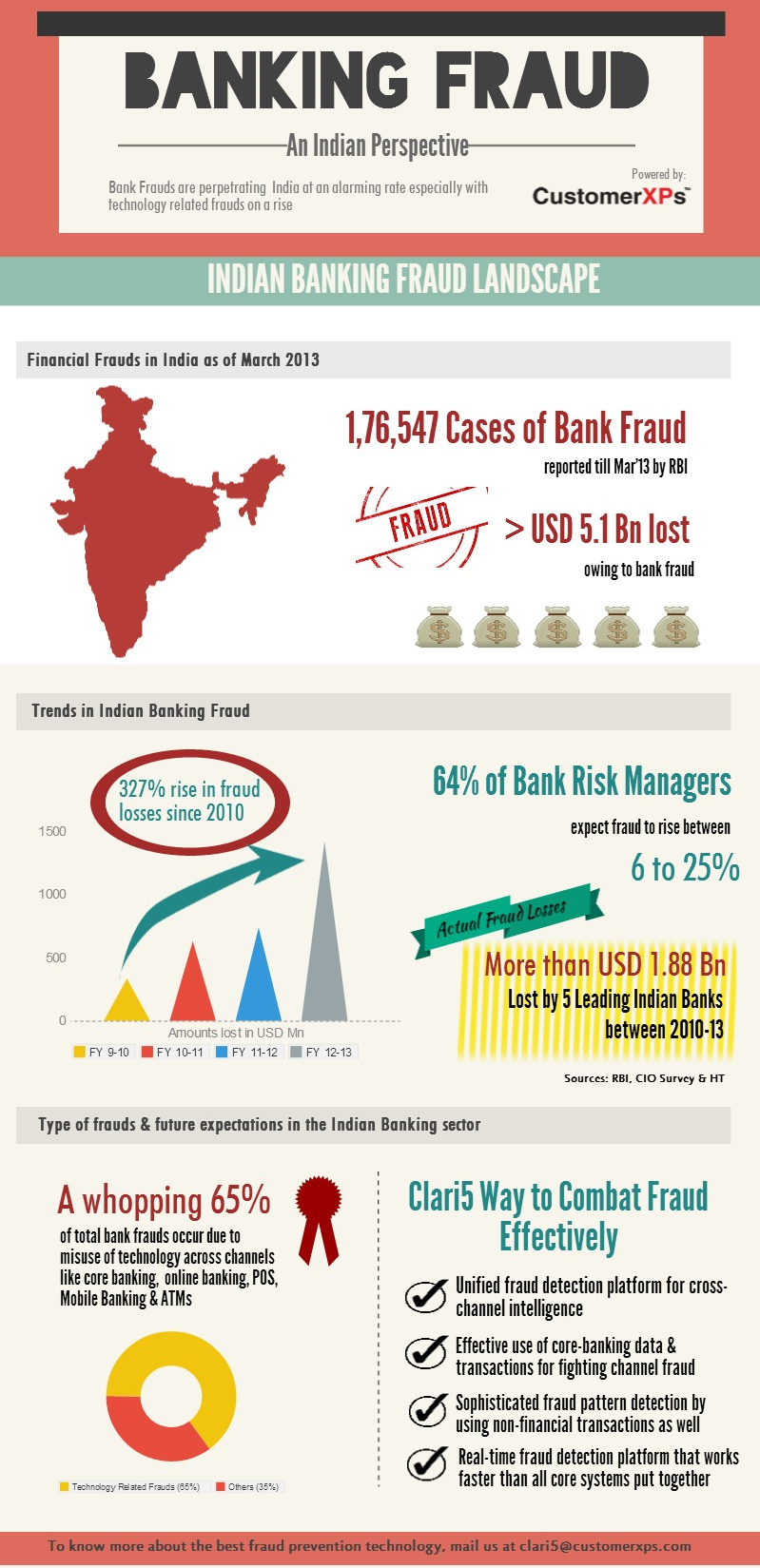

Changing the Indian Banking Fraud Landscape with Real-time Fraud Prevention Technology

Banking fraud is a $3.5 Trillion global menace. Indian Banking Fraud number instances have increased considerably over the past few years. This surge in banking fraud has not only resulted in banks losing millions but also sustaining irreparable reputational damage. With such attacks becoming more frequent, RBI has mandated banks to comply with recommended measures to secure the technology infrastructure and improve fraud risk management practices for frauds across channels. There is thus a growing need for banks to incorporate strong combat mechanism for not only detecting but preventing frauds in real-time.

The infographic below highlights recent trends in the Indian Banking fraud landscape and how implementing real-time fraud management technology would combat such frauds in a fool-proof way.

E-banking, or online banking as we call it, has become an accepted norm of financial transactions for millions around the world. The pervasiveness of internet has contributed to this channel of banking gaining prominence not only in developed countries but also in the developing ones. The modern banking customer who is short on time does not hesitate to log on to her online banking account and make payments online or transfer money, much to her relief. Aren’t we lucky enough to experience such luxury at the hands of technology?

Well, pause for a second. The growing menace of fraud has posed a big threat to the safety of these banking transactions. Identity theft, phishing & smishing (phishing through mobile phones) are the most common fraud practices threatening the online banking space. According to a report published by Kaspersky in 2013, online fraud is costing the global economy many times more than initial estimates of USD 100bn a year, with bank fraud contributing the maximum. Also with the emergence of various social media channels, fraudsters have upped their ante. As per a research by Microsoft, phishing via social networks was used in 84% of the total attacks carried out in 2011. Such attacks not only expose gaps in the online banking ecosystem but also pose a grave challenge for banks- in how to establish a counter-attack mechanism.

Banks must incorporate a strong combat mechanism- that cannot be achieved by simply following an outside-in defense approach that is reactive in nature. What banks need is an inside-out approach to fraud prevention using customer behavioral intelligence. Customer behavioral intelligence not only makes use of financial transaction patterns but also non-financial transaction patterns, user login patterns and device usage patterns to come out with fraud-risk advice. This includes using 2-factor authentication to restrict the fraudster from making unauthorized access into the customer’s online banking account, as mandated by Reserve Bank of India, recently. This fraud-risk advice being available in real-time empowers the banking system to allow, decline or challenge suspicious transactions thereby preventing the internet banking fraud from actually taking place.

Thus, implementing strong online fraud prevention technology is essential not only for making internet banking transactions fraud-proof for customers but also enjoyable. A good fraud prevention solution can not only benefit the bank in terms of improved customer loyalty but also help the bank improve its bottom-line.