Alarming revelations on money laundering and banking frauds have emerged in recent reports by Deloitte, Thomson Reuters and PwC, who comprehensively surveyed MENA (Middle East & North Africa) nations. While the findings have helped financial institutions in improving resourcing, benchmarking and streamlining regulatory compliance, it has also highlighted certain pertinent concerns.

Here are the top five takeaways from these reports.

- From blame game to action

- Prominent since the last few years, the scenario has changed (from where higher authorities were blamed for ineffective action) towards regulatory compliance. The organization as a whole has moved to action mode, where the focus has changed to better customer due diligence, and leveraging technology to fight money laundering and fraud.

- Not only does it help Financial Institutions effectively monitor all processes, but also improves employee performance by establishing a pervasive work culture in which strong commitment to professional and organizational goals are given importance without disregarding customer satisfaction.

- The reports state that despite people in organizations being well aware of decisions taken at the C-level but implementation of the same seems to be lopsided. Short-term lucrative solutions that are often preferred over sound regulatory compliance stand as a major hurdle to the active application of best practices.

- Implementation of ideal resources at present is one of the toughest strategies in battling financial crime in MENA. Lack of substance in this approach has resulted from the predicament of compliance managers who have to adhere to the latest regulatory standards and at the same time be answerable to management for increased resource utilization.

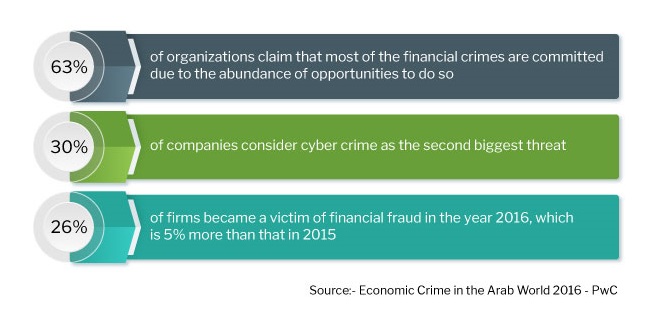

- PwC reports more than 20% of financial institutions in MENA have not even carried out compliance assessment programs. This means 1 in 6 financial institutions will eventually experience enforcement actions by regulatory bodies.

- Higher investments in sophisticated technologies

- Technology has become the most preferable option for almost every bank owing to the tediousness of the job of maintaining evolving regulatory standards and dealing with threats posed by fraudsters at the same time. Cybercrime ranked second on the list of major threats.

- While the cybercrime rate in MENA has reduced by about 7% over 2 years, it still continues to be one of the prominent causes of IT expenditure.

- Process reorg

- Reorganization and updating of processes is the first investment target for financial institutions. Unless all the processes in a financial institution aligned with internationally approved best practices, meeting compliance requirements will be a costly and time-consuming affair. Risk and compliance thus have become the core of enterprise operations in MENA.

- Once implemented effectively, re-designed processes can help decrease the likelihood of money laundering and several other financial crimes. Although immensely difficult to achieve, especially in prominent businesses where work cultures are strongly established and older practices have prevailed, these changes are crucial for organizations to combat financial crime.

- Declining confidence levels in existing/current compliance strategies

- In 2015, close to 50% of respondents to a survey confidently said that the odds of compliance strategies succeeding are pretty high. Last year, however, only about 6% seemed to be highly optimistic about the same, while 44% had little or no confidence. The steadily declining confidence levels in these strategies are certainly going to make it harder to implement them.

- Impediments to policies

- The top concern till very recently for banks in MENA was reputation. Now the worry is more about regulatory requirements. Possibility of failure in meeting regulatory standards, both local and international, has now occupied the minds of both entrepreneurs and those working in compliance management area.

- Another major concern is the fear of inadvertent involvement in financial crime activities. Policies in these financial institutions as a result, have been being stalled. Statistics show that around 37% are concerned about compliance with regulatory standards, while 13% are worried about the internal risks that restrict organizations from meeting regulators’ expectations.

- Another discovery from the Sanctions and Financial Crime Symposium by EY MENA in Dubai, which was attended by over 300 participants combining financial institutions and risk management professionals, is that around 64% of business leaders have an economic crime risk assessment program in place, while about 20% are yet to conduct the same.

These facts serve as an eye-opener for financial institutions in MENA nations. With the nature of financial crimes having become more complex and difficult to detect, the time is right for re-examining current defense strategies and articulating unconventional mechanisms to prevent loss from fraud.

Time for action

- Speed and precision are the critical cornerstones of fraud prevention. Instead of managing multiple channels individually, banks need to establish a system that can function like the human brain. A system that uses fuzzy logic that quickly summons and synchronizes collective wisdom from across all the channels, understands the context and deliver split-second interventions.

- In a rapidly changing regulatory landscape, a pro-active and ‘future-proof’ fraud risk management and AML strategy provides agility and predictability for upcoming regulatory compliance mandates.

- Harness the combined power of current technologies such as AI, ML, Decision Sciences and Real-time Decisions to have a single integrated real-time anti-fraud + AML strategy.

- With ‘digital’ being the mantra of the day, implement an anti-fraud strategy that dovetails with digital. Banks must understand that fraud management and topline growth are two sides of the same coin. The same real-time intel that prevents fraud can be monetized for generating revenue for the bank.

- Only a fraction of banking transactions are actually fraudulent. New age anti-fraud solutions understand transactional behavior patterns, which in turn help banks engage customers better and profitably.

- Step up the fight against fraud to a regional level. A federated approach, specifically a pan-MENA anti-fraud network can be a useful strategy to consolidate, cross-pollinate and share intel among banks in the region.

Sources –

- Financial Crime In The Middle East And North Africa 2016: The Need For Forward Planning – Thomson Reuters & Deloitte

- Financial Crime In The Middle East And North Africa 2016: The Need For Forward Planning – Thomson Reuters & Deloitte

- Adjusting the Lens on Economic Crime in the Arab World – PwC

- Financial Crime Compliance Seen Rising in MENA – Trade Arabia